Publications

Selected peer-reviewed publications with open-source code. Click a title for papers, code, and details.

2026

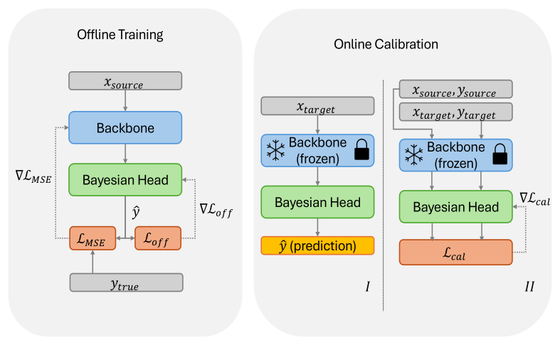

"Model-Agnostic Online Certificate-Driven Calibration for Time Series Forecasting

Under Distribution Shift"

UAI 2026 Oral

Under Distribution Shift"

Time series out-of-distribution generalization requires forecasters to remain reliable when deployment dynamics differ from training conditions due to covariate shift, concept shift, and temporal dependence. Probably Approximately Correct Bayesian domain adaptation provides computable certificates by decomposing target risk into a source risk term, a source-to-target mismatch term, and a complexity term, but standard analyses rely on independent sampling and distributional stability, assumptions that are violated in time series by serial dependence and nonstationary shift. We propose a model-agnostic online martingale Probably Approximately Correct Bayesian framework that yields finite-sample certificates under temporal dependence and distribution shift. The certificate replaces independent-sample concentration with martingale concentration that adapts to loss scale and predictable variation. We use the certificate as a surrogate regularizer for online calibration by training a gated residual Bayesian head on top of a fixed forecasting backbone, producing a corrective update that reverts to the backbone prediction when the gate is closed. Online calibration combines a source risk anchor, a posterior-shift penalty, and a time-adaptive mismatch term computed from target windows observed before forecasting. It follows a predict-then-update protocol in which outcomes become available only after forecasting and are used to update subsequent predictions. Experiments across convolutional, attention-based, and large language model-based forecasters show improved stability and accuracy under covariate and concept shift.

"PAC-Bayesian Meta-Learning for Few-Shot Identification of Linear Dynamical Systems"

TMLR 2026

Identifying linear time-invariant (LTI) dynamical systems from data is especially challenging when trajectories are short, noisy, or high-dimensional. Traditional system identification methods typically treat each system in isolation and therefore fail to exploit shared structure across related systems. We propose a PAC-Bayesian meta-learning framework for few-shot LTI system identification (PBML-LTI), which learns a transferable prior over task-specific dynamics while preserving task-level heterogeneity. Each task corresponds to an unknown LTI system, and a meta-learner uses a collection of training trajectories to learn a data-dependent prior over transition matrices. Given a new system with limited trajectory data, PBML-LTI performs Bayesian adaptation under the learned prior to produce a task-specific posterior, yielding both accurate point estimates and principled uncertainty quantification in the few-shot regime.

A key technical challenge is temporal dependence: trajectories generated by LTI systems violate the i.i.d. assumptions underlying most existing PAC-Bayes analyses for meta-learning. To address this, we develop a martingale PAC-Bayes analysis for dependent trajectory losses and use it to motivate a fit–KL surrogate objective for meta-training. The resulting support–query predictive-risk bound clarifies how empirical fit, posterior complexity, and prior quality interact in few-shot adaptation under sequential dependence. We further show how this predictive bound induces problem-specific corollaries for transition-matrix recovery and multi-step trajectory prediction. Together, these results connect uncertainty-aware meta-identification with finite-sample analysis for dependent dynamical data.

A key technical challenge is temporal dependence: trajectories generated by LTI systems violate the i.i.d. assumptions underlying most existing PAC-Bayes analyses for meta-learning. To address this, we develop a martingale PAC-Bayes analysis for dependent trajectory losses and use it to motivate a fit–KL surrogate objective for meta-training. The resulting support–query predictive-risk bound clarifies how empirical fit, posterior complexity, and prior quality interact in few-shot adaptation under sequential dependence. We further show how this predictive bound induces problem-specific corollaries for transition-matrix recovery and multi-step trajectory prediction. Together, these results connect uncertainty-aware meta-identification with finite-sample analysis for dependent dynamical data.

2025

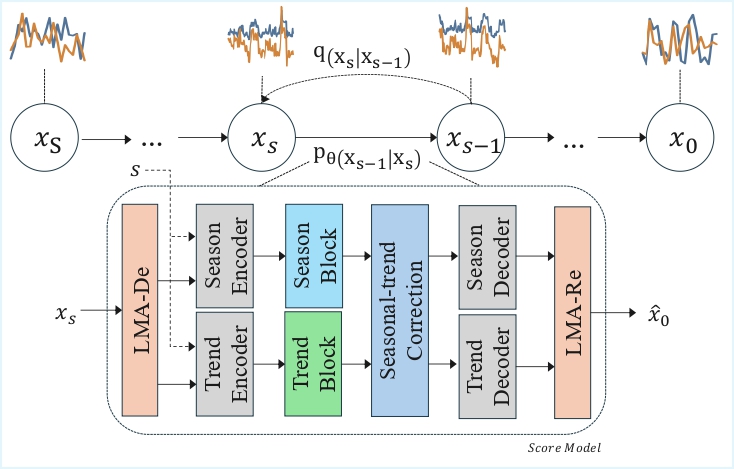

We introduce STDiffusion, a generative framework for time series that explicitly

decomposes each sequence into trend, seasonal and stochastic components. A

lightweight decomposition module produces component-wise representations; dedicated

component learners capture long-term trend and periodicity, while a diffusion

backbone models residual innovations conditioned on those components. This design

yields faithful, structure-aware samples and enables controllable generation and

augmentation for downstream forecasting tasks. The figure below shows the

overall architecture.